berbagiberkat.com – The Presidential Cycle (also known as the Presidential Election Cycle Theory) is a well-known seasonal pattern in financial markets that links U.S. stock market returns to the four-year term of a U.S. president. First popularized by Yale Hirsch in the 1960s through his Stock Trader’s Almanac, the theory suggests that stock performance follows a somewhat predictable rhythm tied to political incentives, policy implementation, and election-related sentiment—regardless of the president’s political party.

The core idea is simple: presidents and their administrations tend to behave differently across the four years of a term, influencing economic policies, spending, and investor psychology in ways that create recurring market tendencies.

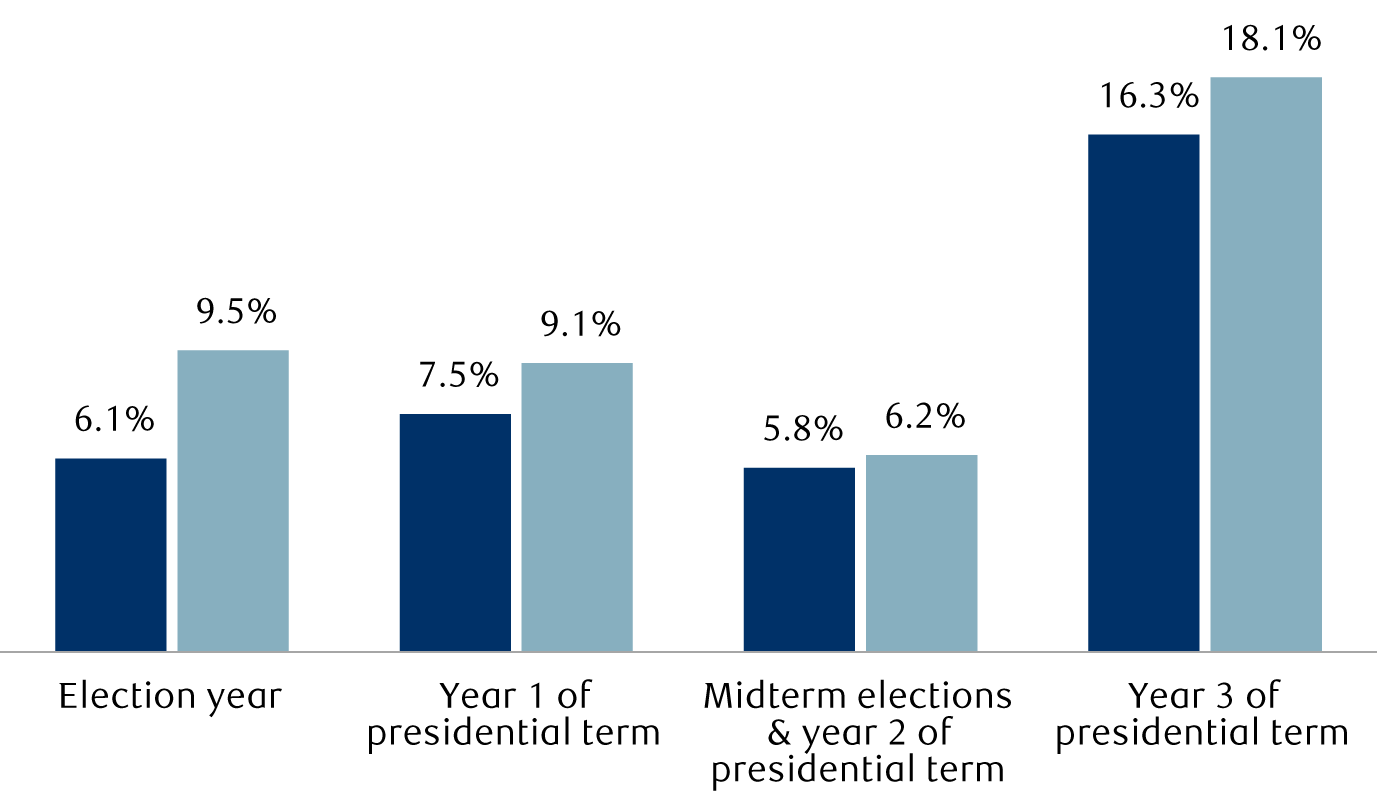

The Four Phases of the Presidential Cycle

The cycle resets every four years, starting with the year a president takes office (post-election year). Historical averages (often based on S&P 500 or Dow Jones data from the mid-20th century onward) show this typical pattern:

- Year 1: Post-Election Year Often the weakest or most mixed year. New administrations implement campaign promises, which can include unpopular measures (tax hikes, spending cuts, or regulatory changes) to address inherited problems. Uncertainty about the new leadership leads to cautious investor behavior.

- Historical average S&P 500 return: Around 3–7% (varies by dataset), but frequently below the long-term norm.

- Year 2: Midterm Year Traditionally the weakest phase overall. Midterm congressional elections create political gridlock and uncertainty. Presidents may face opposition Congress, forcing compromises or stalled agendas. Markets often experience higher volatility and lower average returns.

- Many analysts note this as the riskiest year, with potential for corrections or bearish periods leading into midterms.

- Year 3: Pre-Election Year Historically the strongest year by far. Incumbent presidents (or their party) ramp up stimulative policies—tax cuts, infrastructure spending, deregulation—to boost the economy and improve re-election chances (or support their party’s nominee). Investor optimism rises as growth accelerates.

- Average S&P 500 gains often exceed 10–15% in many historical analyses, making this the standout phase.

- Year 4: Election Year Performance is solid but usually less explosive than Year 3. Early uncertainty from campaigns gives way to relief rallies once uncertainty resolves (post-election). Markets tend to rise in the second half, especially if pro-business policies are anticipated.

- Average returns: Around 6–11%, often positive but tempered by volatility around primaries and the November vote.

This pattern is attributed to political incentives: the further a president is from the next election, the more willing they are to take tough (potentially market-negative) actions. Closer to re-election, stimulus and positive economic optics dominate.

Historical Evidence and Performance

Data from sources like the Stock Trader’s Almanac, Ned Davis Research, and Charles Schwab (covering periods from the 1920s/1950s to recent decades) generally support the pattern, especially the dominance of Year 3:

- Since the mid-20th century, Year 3 has delivered the highest average returns (often 10–15%+ for the S&P 500).

- The cycle has shown consistency across both Democratic and Republican administrations—suggesting it’s driven more by electoral timing than ideology.

- From 1928–2024, the S&P 500 rose in about 78% of pre-election years (Year 3), compared to ~67% in all calendar years overall.

However, the pattern is not foolproof:

- It weakened or inverted in parts of the 21st century (e.g., strong Year 1 gains under Obama, Bush, and Trump presidencies).

- Major external shocks (COVID-19 in 2020, financial crises) can override the cycle.

- Recent years have seen debates about whether increased market efficiency, Federal Reserve dominance, globalization, or structural changes have diminished its reliability.

Relevance in 2026

As of January 2026, we are in Year 2 of Donald Trump’s second non-consecutive term (inaugurated January 2025). According to classical theory, this midterm year is historically the weakest, with potential for volatility, corrections, or subdued gains ahead of the 2026 congressional midterms.

Analysts’ views vary:

- Some warn of possible “bear market action” or significant intra-year pullbacks due to midterm uncertainty, policy crosscurrents, and historical seasonality.

- Others note that post-2025 momentum (strong 2025 performance) and factors like AI-driven growth could mitigate weakness.

- Wall Street S&P 500 targets for end-2026 range widely (e.g., 7,100–8,100), implying modest single-digit returns at best—below long-term averages.

Limitations and Investor Takeaways

The Presidential Cycle is a statistical tendency, not a guaranteed rule. Markets are influenced far more by earnings growth, interest rates, inflation, geopolitics, and technological shifts than by election calendars alone. Many experts advise against using it as a standalone timing tool—past patterns do not predict future results with certainty.

Still, it remains a useful framework for understanding sentiment and risk at different points in a presidential term. Awareness of the cycle can help investors prepare for potential volatility (especially in Years 2 and early Year 4) while recognizing that the strongest seasonal tailwinds often arrive in pre-election years.

In short, the Presidential Cycle reminds us that politics and markets are intertwined—not because presidents “control” stocks, but because their incentives shape economic policy and investor psychology over a predictable four-year rhythm.